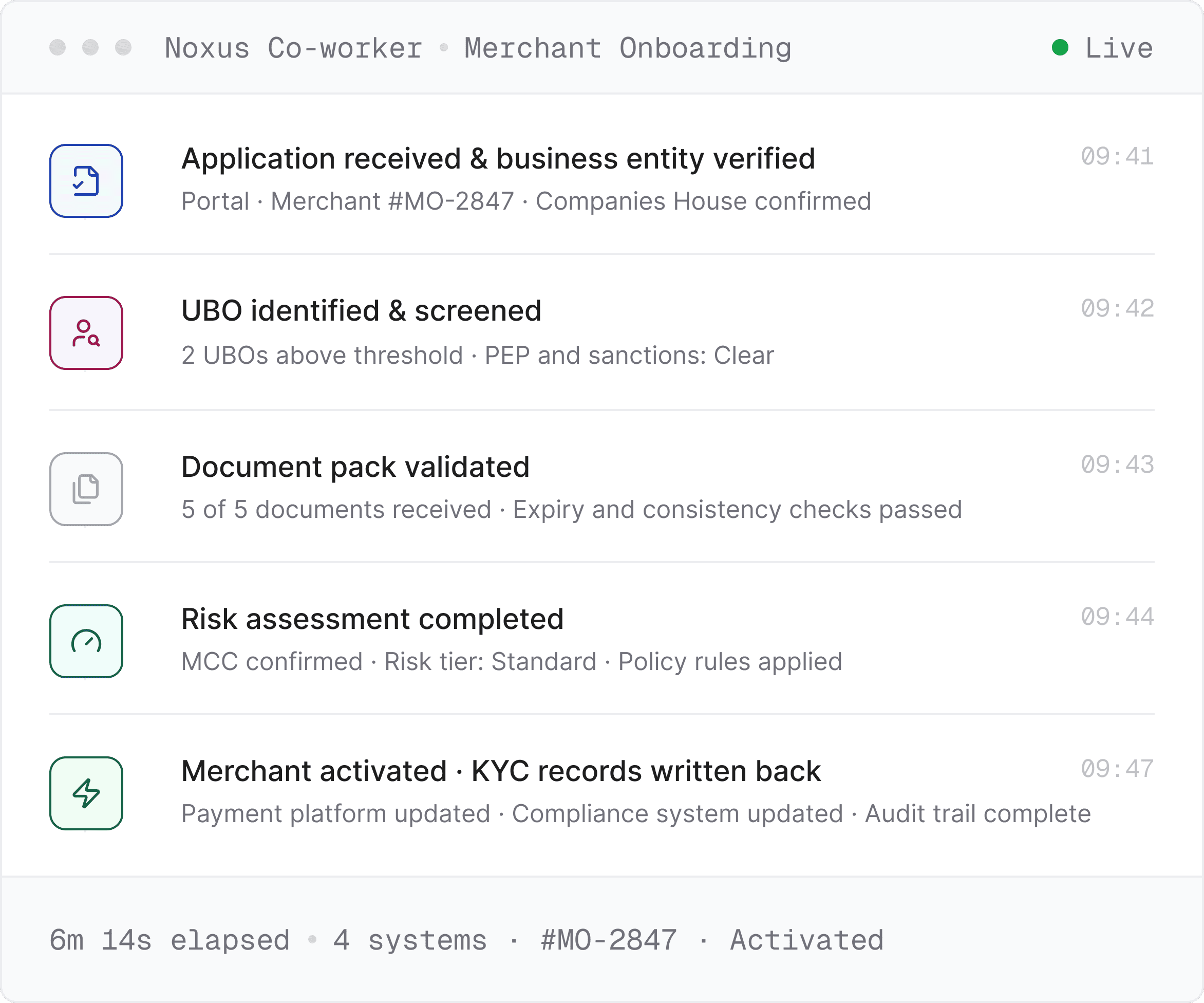

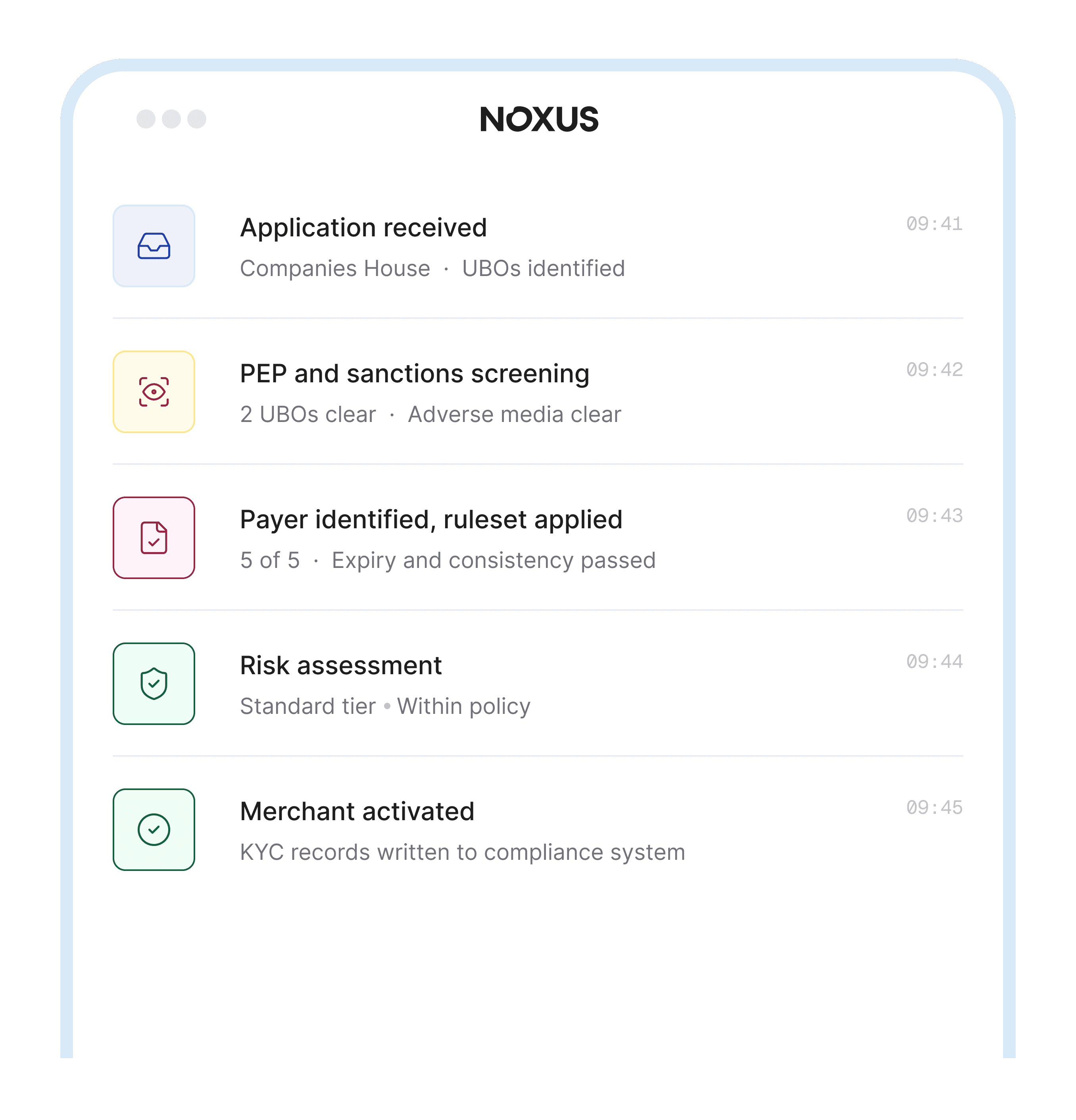

Every merchant application triggers a manual chain of verification, screening, and document review before the merchant can transact

Today

Operations team

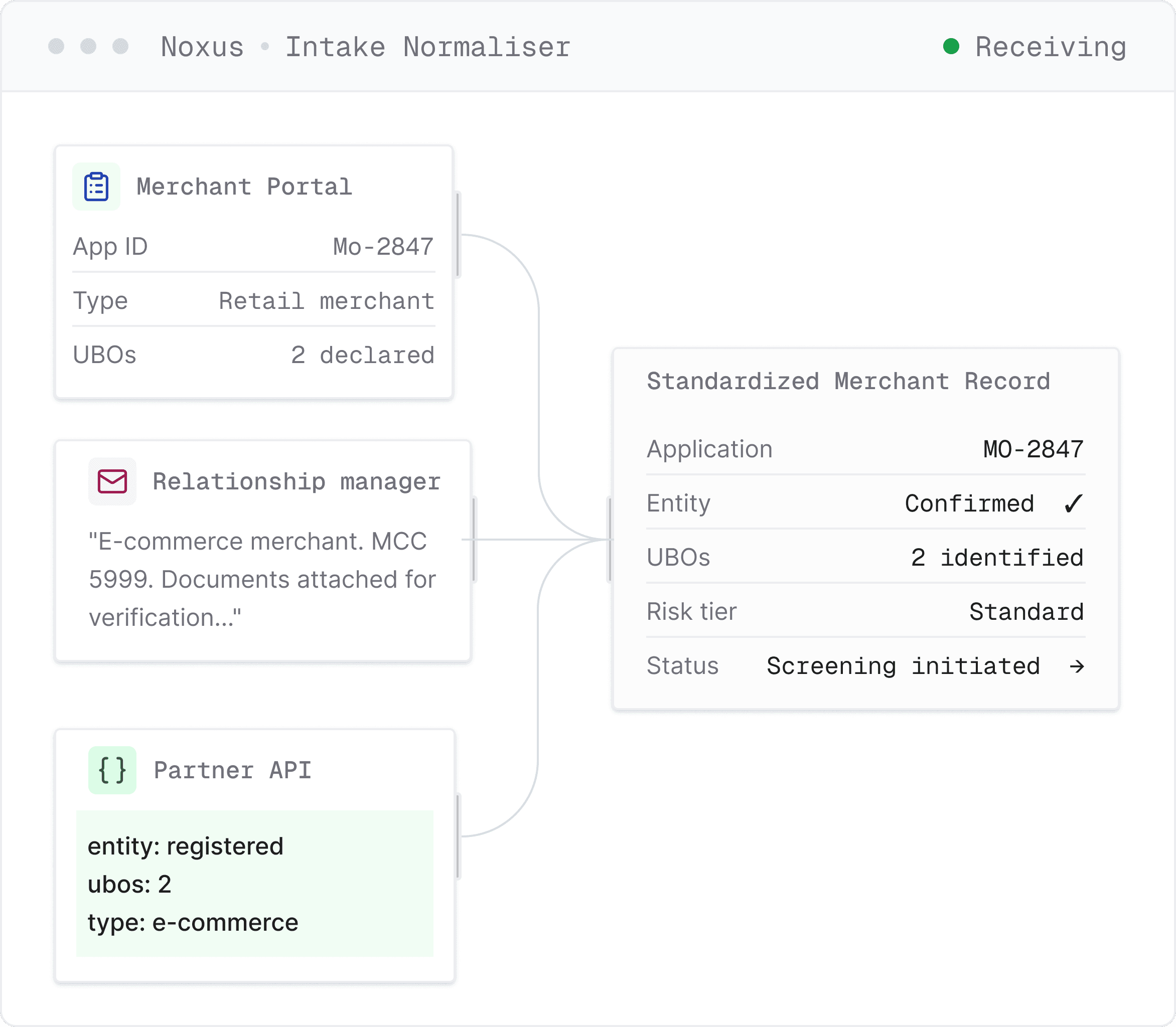

Applications arrive across channels and logged manually

Business entity verified manually against the registry

UBOs identified manually from the ownership structure

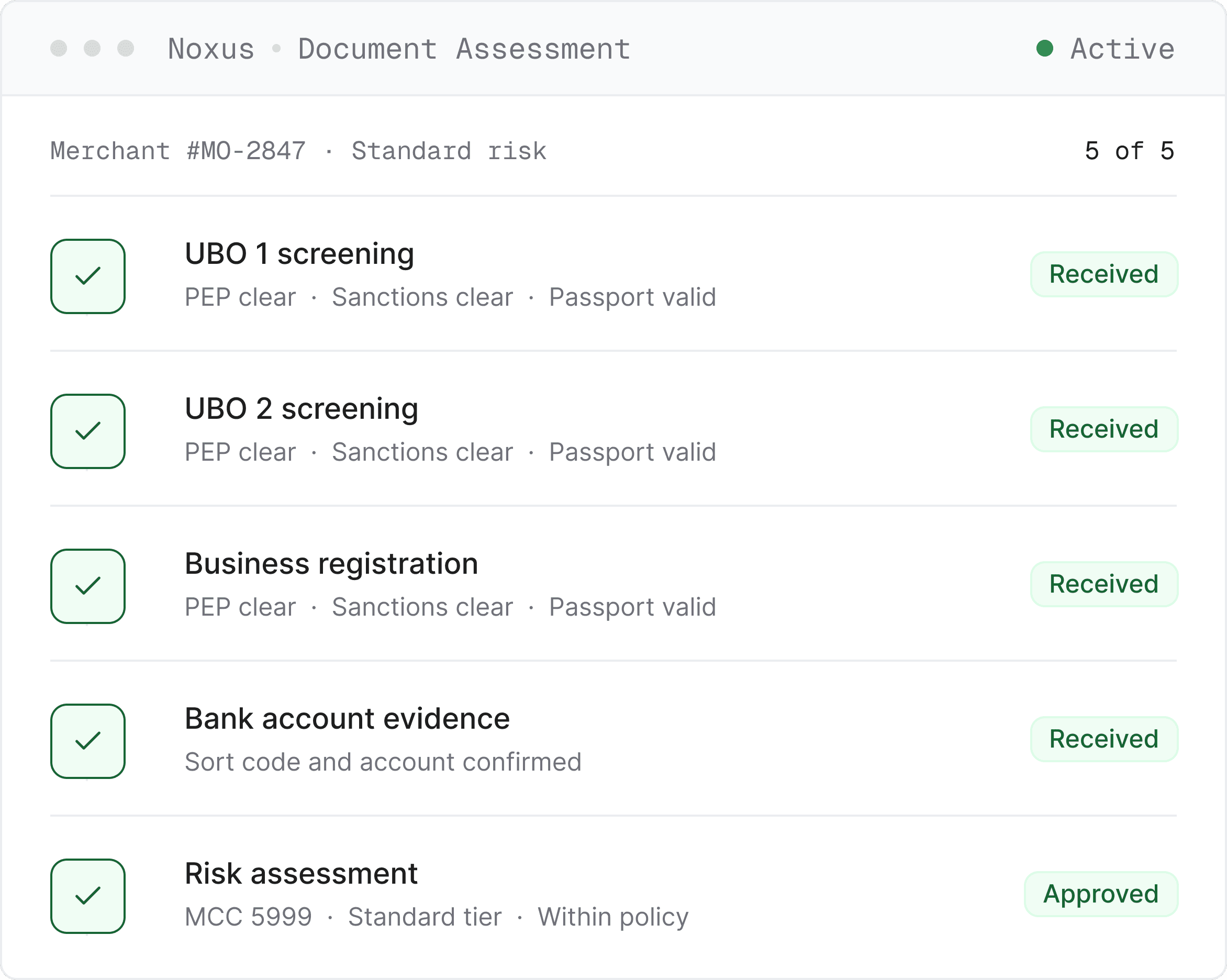

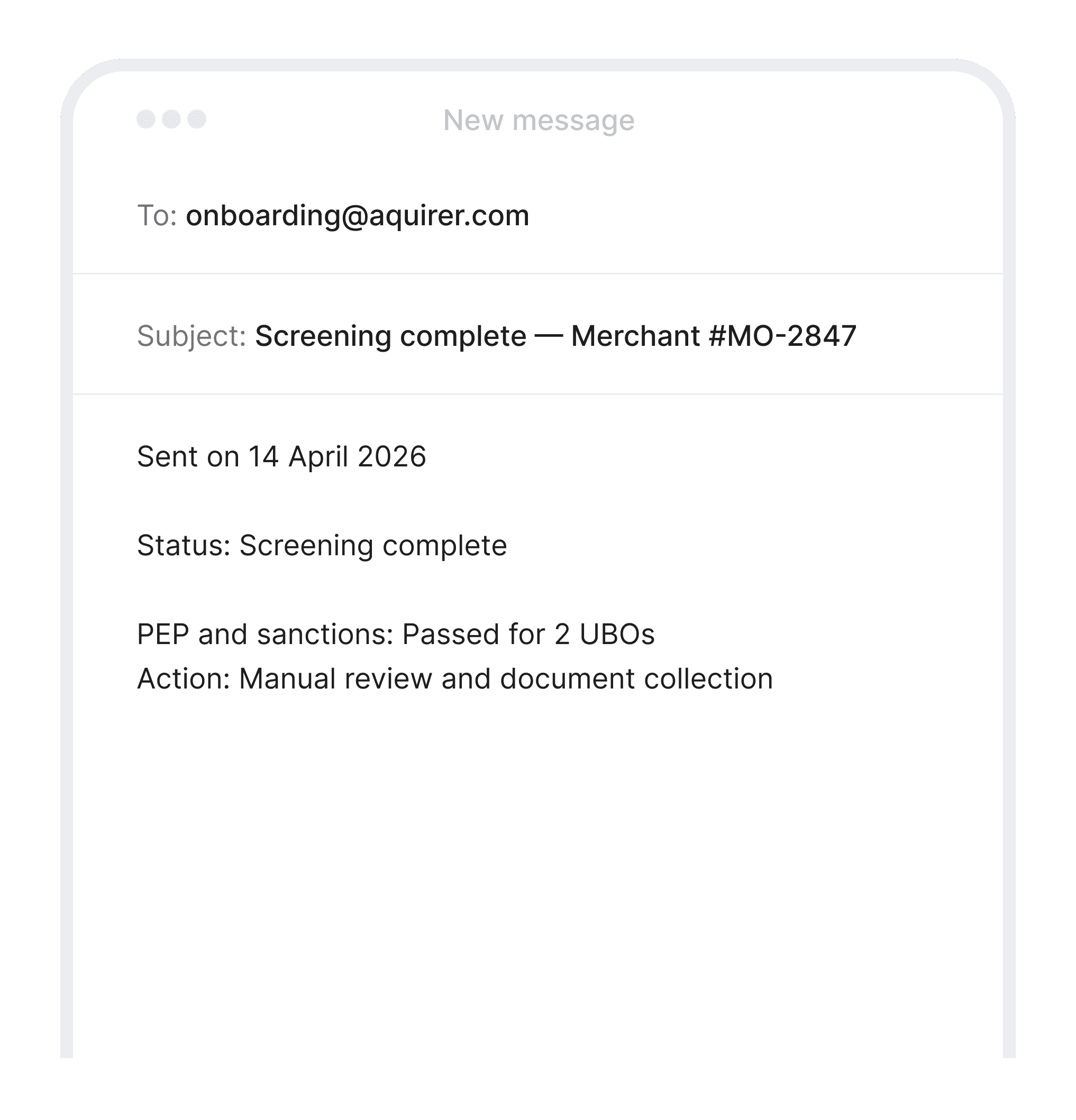

PEP and sanctions screening run manually per UBO

Risk assessment run manually against the acquirer's policy

With Noxus

Co-worker

Every channel feeds a single governed KYC verification workflow

Business entity verified automatically with address and name matched

UBOs above the ownership threshold identified automatically

PEP and sanctions screening run with adverse media checks

High-risk categories flagged at classification before screening begins

How Noxus Works

Three layers powering merchant onboarding and KYC verification

Connects to your payment platform, compliance system, and registry - running intake, UBO screening, document validation, risk assessment, and merchant activation end to end.

01

Onboarding Intelligence

Receives applications from any channel, verifies the business entity, identifies UBOs above threshold, and flags high-risk merchant categories before screening.

RECEIVE

→

VERIFY

→

CLASSIFY

02

Autonomous Execution

Runs PEP and sanctions screening per UBO, validates documents, applies the risk policy, and activates approved merchants.

VALIDATE

→

ASSESS

→

ACTIVATE

03

Governance and Audit

Every step logged - UBO screening, document validation, and risk assessment. Complete KYC audit trail written to the compliance system.

LOG

→

REPLAY

→

REVIEW

Capabilities

What happens across each layer of the merchant onboarding and KYC verification workflow

Business entity verified against the registry. UBOs identified from the ownership structure. High-risk MCC codes flagged at classification before screening begins.

PEP and sanctions screening runs per UBO with adverse media checks. Documents validated and gaps chased automatically. Standard merchants activate straight through. Elevated-risk cases route with the complete file assembled.

Every step logged - business verification, UBO screening, document validation, and activation. No merchant activates without a complete KYC record. Available for regulatory and AML review.

agentic operations

Onboarding effort belongs on merchant activation

Correct activation means verifying the business entity, screening every UBO, validating documents by risk tier, and writing a complete KYC record to the compliance system.

Verifies, screens, validates, and activates automatically

Built for Every Team

Noxus works across every role in the merchant onboarding and KYC verification workflow

Operations & Merchant

Standard-risk merchants verified, screened, and activated without manual involvement. The team focuses on elevated-risk cases - each arriving with the full file ready.

Compliance

Every merchant produces a complete KYC record - verification, UBO screening, document validation, and risk assessment - available for regulatory inspection and financial crime review.

IT and Architecture

Deploy on your existing payment platform and compliance system - no API prerequisites or middleware projects. Noxus connects to leading platforms and registry interfaces natively.

Measured results

Numbers that move the business

Measured outcomes from merchant onboarding deployments on existing payments and compliance stacks.

What Customers Say

Trusted by teams running the operations

Frequently Asked

Questions about Merchant Onboarding & KYC Verification

How quickly can KYC verification software be live?

6-8 weeks from contract to production on live application data. Payment platform connectivity, compliance system integration, and risk policy rule configuration occupy the first phase, followed by parallel testing on live application volume before handover.

What systems does the KYC verification software connect to?

Your payment platform for merchant activation and account write-back; your compliance system for KYC record storage and audit trail; your business registry interface for entity verification; and your PEP and sanctions screening provider. Specific connectors confirmed during scoping.

What happens when a document is missing or invalid?

A targeted request is sent directly to the merchant or relationship manager identifying the specific document required and the reason it is needed. The application is held and resumes automatically when the document is received and validated. No manual follow-up is needed.

How is the UBO ownership threshold applied?

The ownership threshold, typically 25%, is encoded in the workflow configuration. UBOs at or above the threshold are identified from the submitted ownership structure and screened automatically. Where the ownership structure is complex or layered, the case routes to the compliance specialist with the structure and the identified UBOs documented.

What triggers the enhanced due diligence path?

High-risk MCC codes, merchants operating in high-risk jurisdictions, UBOs with PEP status, adverse media hits, and declared transaction volumes above the standard tier threshold. All of these route to the compliance specialist with the complete screened and validated file assembled rather than a blank application.

What does a compliance specialist receive on an elevated-risk case?

The business verification result, the UBO identification with screening outcomes, the document validation status, the specific risk indicators identified, and a structured case summary. The specialist reviews the substance of the risk rather than assembling the evidence from scratch.

Does Noxus make any activation decisions?

No. Activation follows from the acquirer's encoded risk policy applied to the verified and screened merchant record. The AI layer handles application intake, business verification, and evidence assembly. The rules layer governs every approval and activation action. No merchant is activated without a complete KYC record and a policy-compliant approval.

Can this merchant onboarding solution handle different merchant categories and risk tiers?

Yes. Required document packs, screening requirements, and risk assessment criteria are configured independently by merchant category and risk tier. A standard retail merchant runs against different criteria than a high-risk e-commerce merchant or a financial services intermediary.

What makes dedicated KYC verification software different from standard onboarding tools?

Standard merchant onboarding software collects documents and routes them to a reviewer - it was built for intake, not for verifying business entities against registries, identifying UBOs from ownership structures, running PEP and sanctions screening per UBO, validating document packs by merchant category, assessing merchants against acquirer risk policy, and activating in the payment platform with a complete KYC audit trail. KYC verification software purpose-built for this workflow eliminates the manual review loop on standard cases. Merchant onboarding automation software that covers only one step still requires the compliance team to bridge the rest. Noxus runs the full onboarding chain end to end on the existing payments and compliance stack.

How does Noxus compare to other KYC verification solutions and merchant onboarding software?

Screening platforms run PEP and sanctions checks in isolation - they do not verify the business entity, identify UBOs from the ownership structure, validate the document pack by merchant category, assess the merchant against the acquirer's risk policy, or activate the merchant in the payment platform with a complete KYC audit trail. Merchant onboarding solutions that collect documents still require manual verification. KYC verification solutions that run checks still require a human to assess the output and route the outcome. Noxus runs the full onboarding chain end to end on the existing payments and compliance infrastructure.

Ready to automate merchant onboarding and KYC verification on your existing stack?

Live in 6-8 weeks. No API prerequisites. No migration project.